Green Shoots

Bitcoin's bottom is still building, but its character is shifting. Long-term holder capitulation is cooling, buyers absorbed the June lows, and price is climbing back toward the levels that capped it

Executive Summary

- Last week's deep-value read still holds; the change is that the market has started testing the resistance above it.

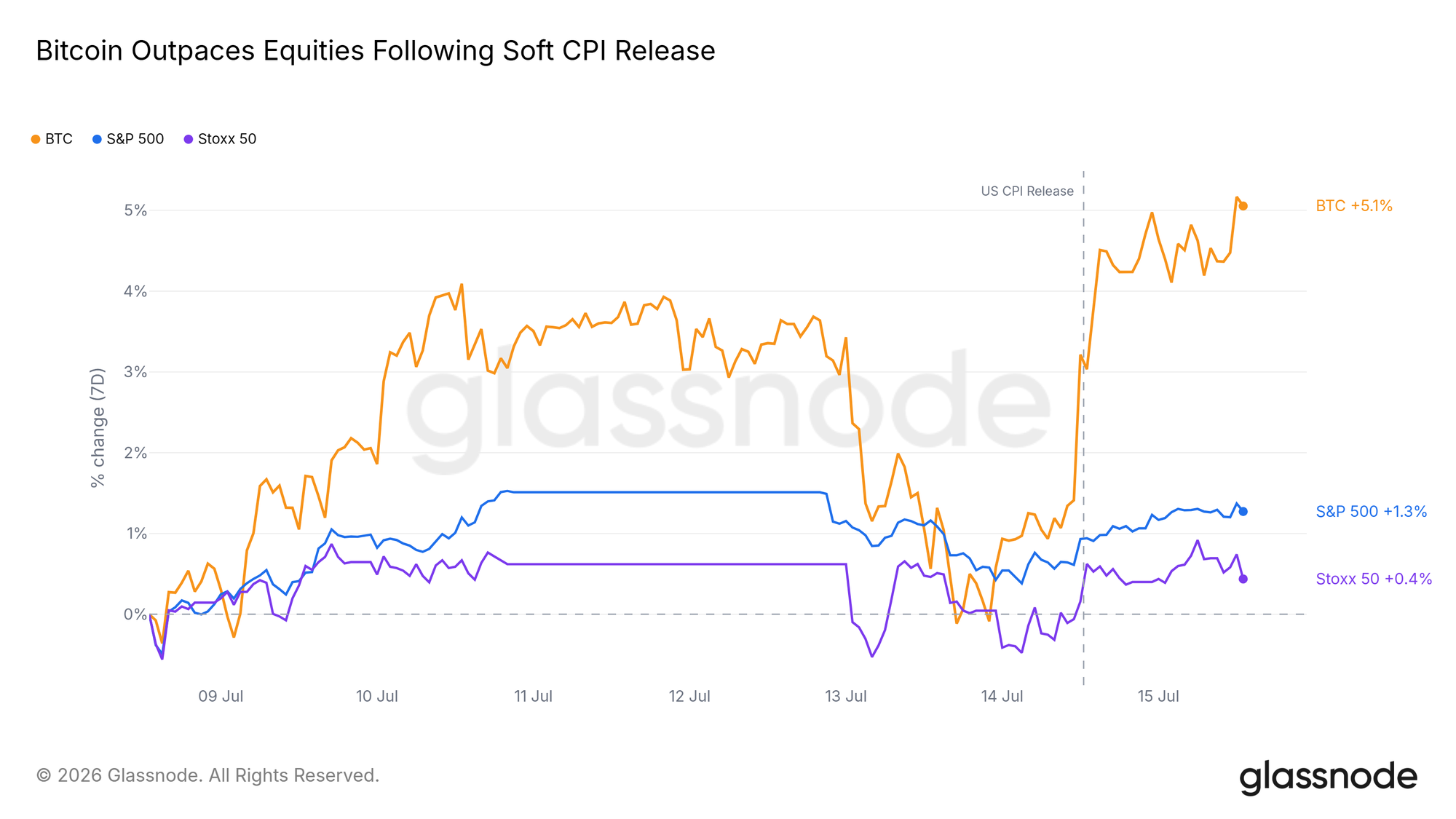

- Bitcoin reacted to the soft inflation print more strongly than any major equity index, its best response to good news in weeks.

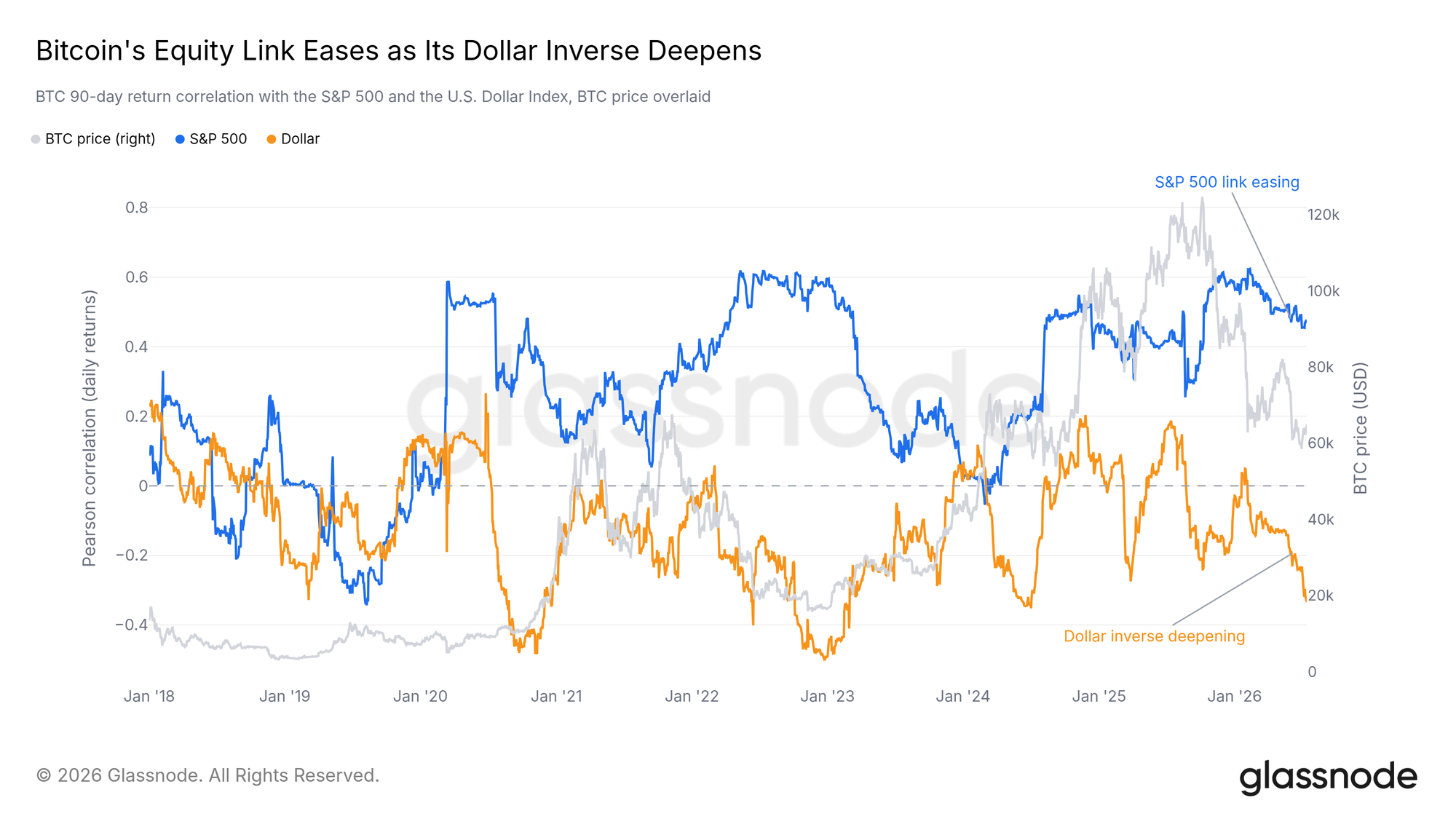

- The tie to equities is loosening while the inverse link to the dollar deepens: liquidity, not risk appetite, is in the driver's seat.

- Long-term holder capitulation, the main source of sell pressure all year, has turned down from its peak.

- Profit-taking has dried up and buyers absorbed the June lows, thinning the supply that met every rally.

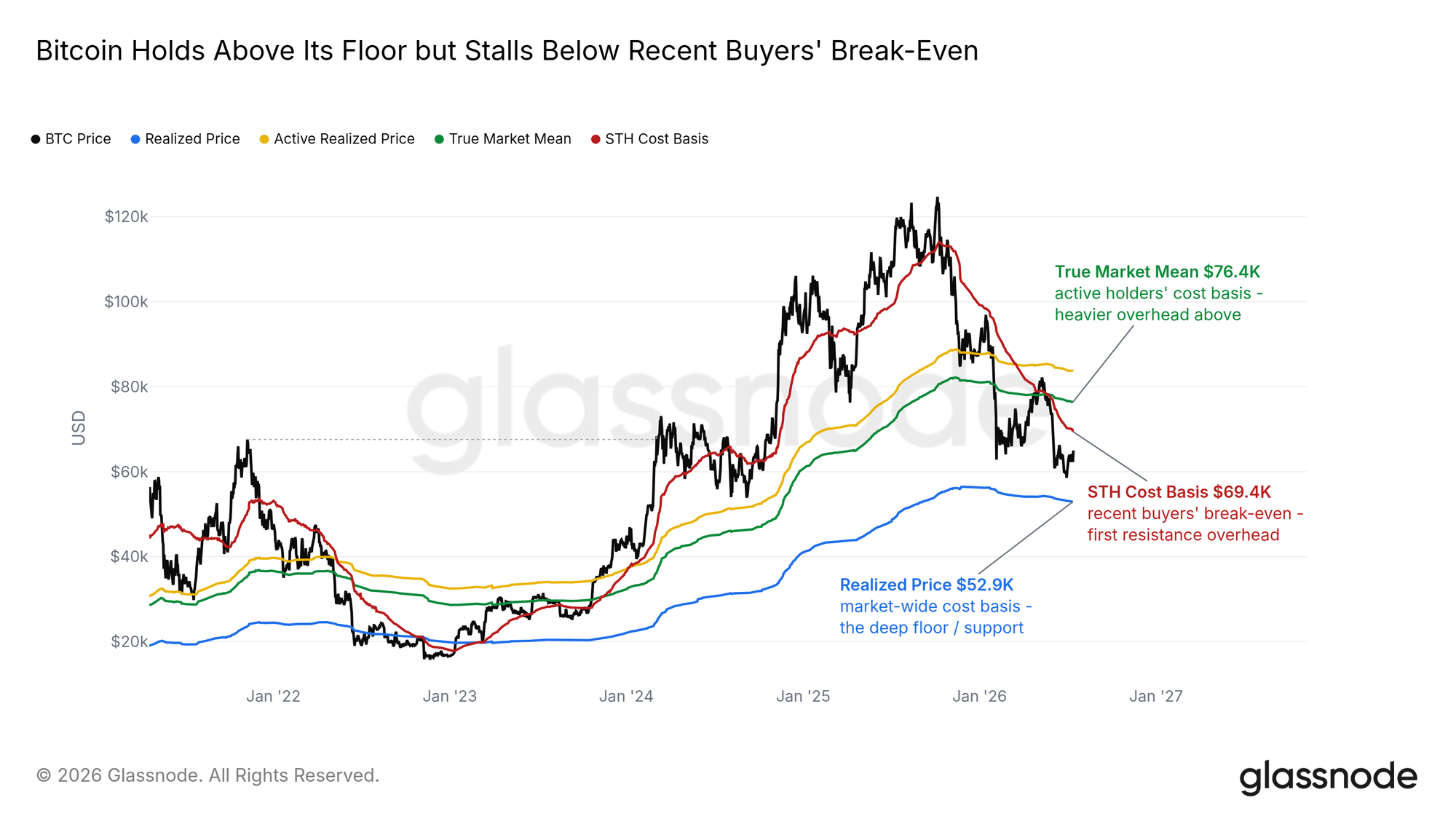

- The Short-Term Holder Cost Basis near 69K, the break-even of recent buyers, is the next overhead resistance; expect a strong reaction there.

- Derivatives traders are unwinding their downside bets, but spot buying has not yet followed. That is the missing piece.

Macro Insight

Bitcoin's pressure this quarter has been a real-rate story, not a risk-off one. Ten-year real yields have climbed to a 2026 high near 2.4%, and the dollar has held above its 200-day average since May. Yet nothing in the broader risk complex is flashing stress: equities sit close to their highs, credit spreads are near their tights, and volatility is subdued.

Bitcoin Leads the Bounce

Tuesday's soft inflation print moved Bitcoin more than any other major asset. It jumped out of the release hour and finished the week well ahead of US and European equities. After a month of grinding sideways near the lows, the market is responding to good news again.

That sensitivity is the tell. A market this eager to rally on one inflation print is a market where sellers are spent and buyers are waiting for a reason.

The Macro Identity Shifts

Beneath the bounce, what drives Bitcoin is shifting. Its correlation with US equities has been easing since the winter, while its inverse relationship with the dollar keeps deepening. Bitcoin trades less like a stock proxy and more like an asset that firms when the dollar weakens.

It has not left the risk complex, but the dollar-and-liquidity channel now matters more than equity sentiment. If macro conditions ease from here, that is the channel most likely to move first.

On-chain Insight

Between Floor and Ceiling

The cost-basis map places this move precisely. Bitcoin trades above the Realized Price, the average price paid across every coin in the market and the natural floor of a bear market. It trades below the Short-Term Holder Cost Basis near 69K, the average entry of buyers from the past five months. The recovery is climbing toward that break-even, its next overhead resistance, with heavier layers of trapped buyers waiting above.

The first meeting with that level will likely draw a strong reaction, because the people most inclined to sell are the ones about to be made whole. A convincing reclaim would give the recovery room to run; a rejection keeps the range intact.

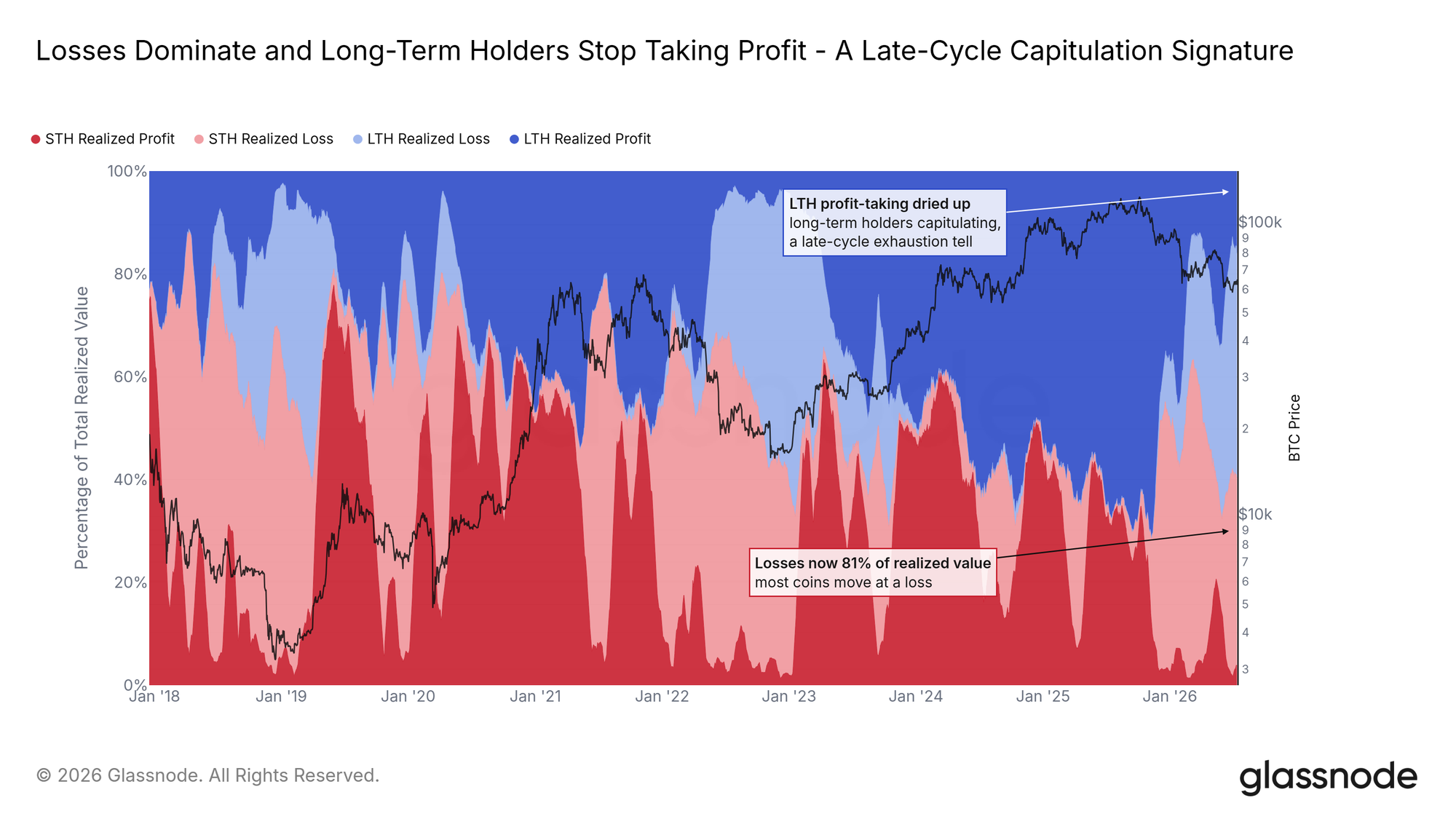

Sellers Stop Taking Profit

The Relative Long/Short-Term Holder Realized Profit and Loss splits everything sold on-chain into four buckets: old hands and recent buyers, each selling at a profit or at a loss. For most of the cycle, long-term holders selling at a profit dominated that mix. That flow has dried up almost completely; what old hands sell now, they sell at a loss.

Losses from both groups make up most of what moves on-chain, the signature of a late-stage bear market. The important change is that the long-term holders' share has stopped growing. The wave of selling that met every rally this year is no longer building.

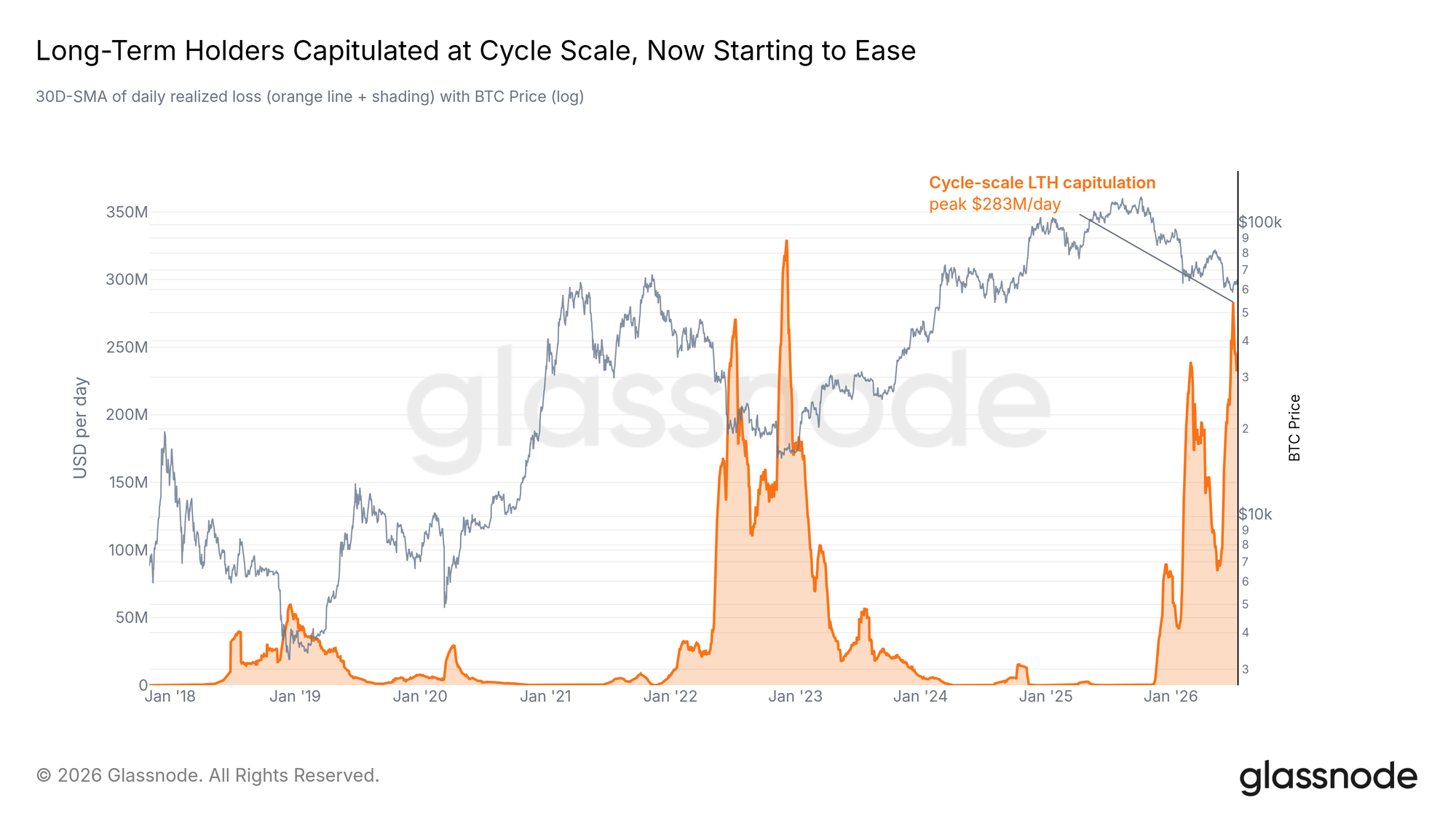

Capitulation Starts to Cool

The pace of that surrender is the most important series on the board. The Entity-Adjusted Long-Term Holder Realized Loss filters out internal transfers and measures what long-term holders actually give up each day. It set its cycle peak two weeks ago, and last week this report named a cooldown in exactly this metric as the precondition for any durable recovery.

It has now turned down. One turn does not prove exhaustion, and a fresh shock could restart it. But for the first time this cycle, the metric that defines the bottoming process is falling instead of rising. The sellers who made this bear market are, at the margin, running out.

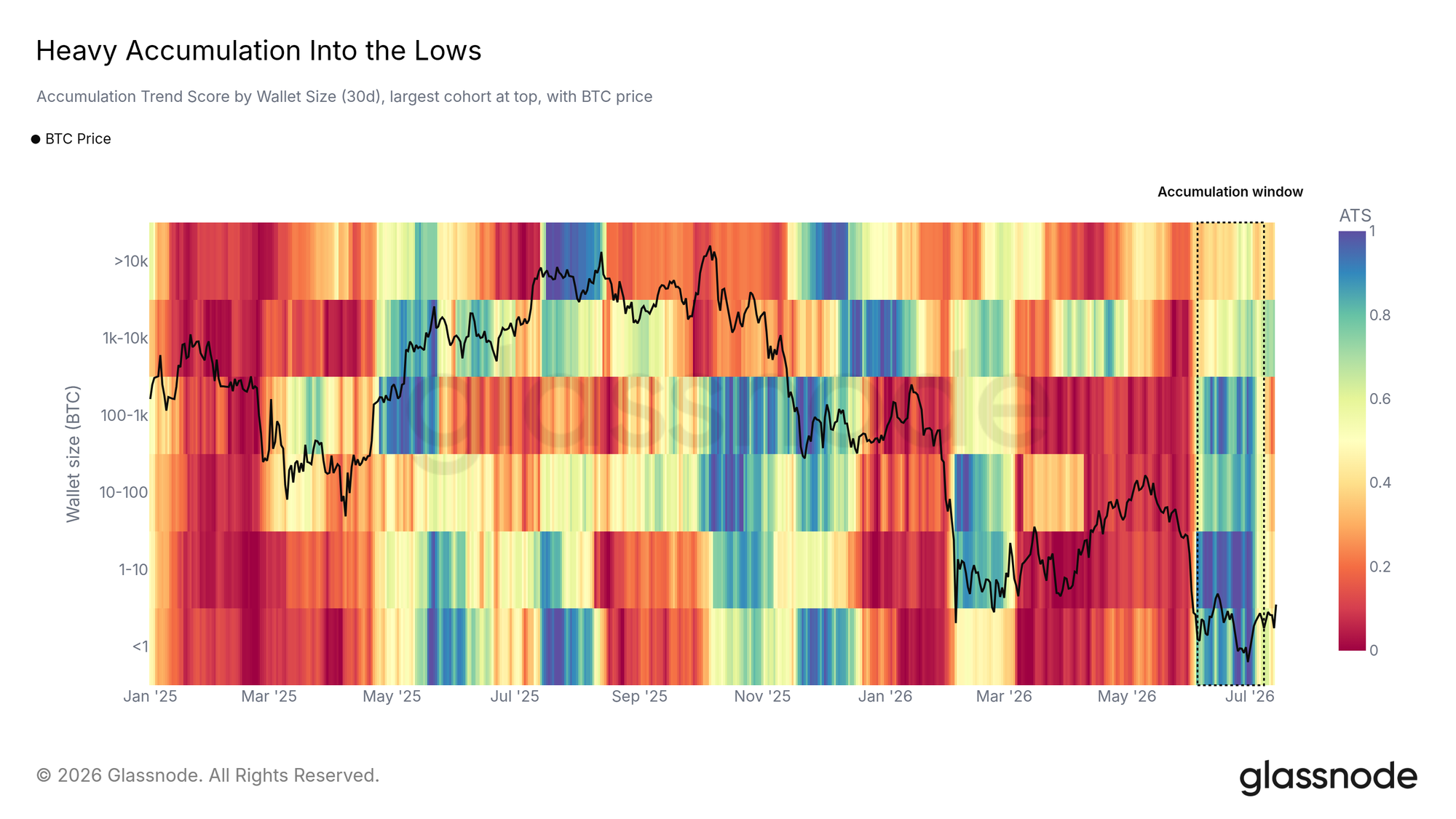

Demand Absorbed the Lows

While old hands surrendered, buyers stepped in. The Accumulation Trend Score by wallet size shows a heavy, broad wave of buying into the June lows, spread across small wallets and large ones alike. Since price stabilized, that intensity has faded and the market has settled into waiting.

The coins sold at the lows found buyers. Whether those buyers return with the same force on the next move decides if this base holds.

Off-chain Insight

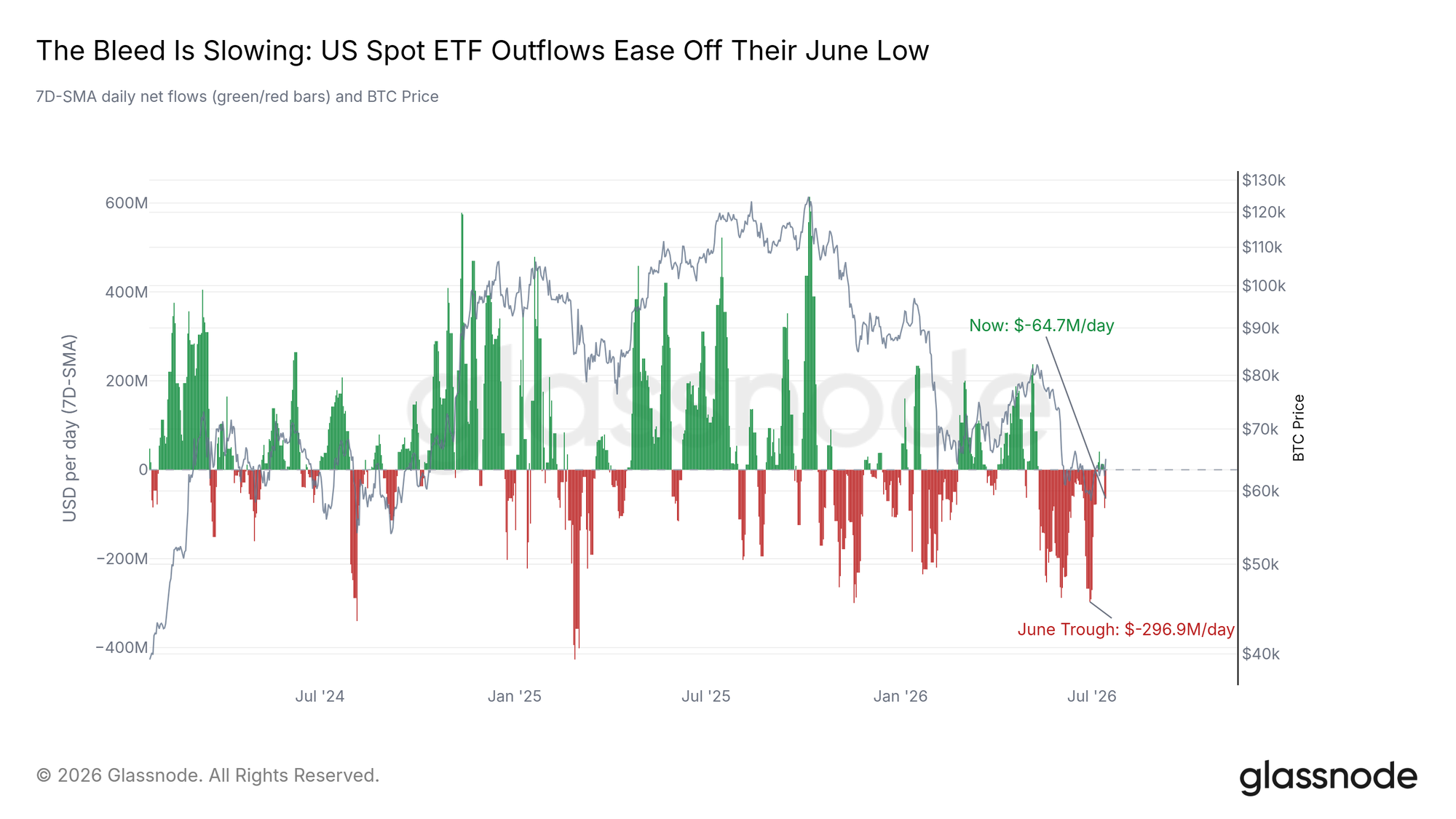

The ETF Bleed Slows

The US spot ETFs tell the same story of pressure easing without resolving. Redemptions have slowed sharply from their June extreme, and the trend points toward stabilization. The channel is not healed, though: one session this week produced the heaviest single-day outflow in weeks before flows partially recovered the next day.

Until inflows return and hold, this remains a market where institutions have stopped fleeing but not started buying.

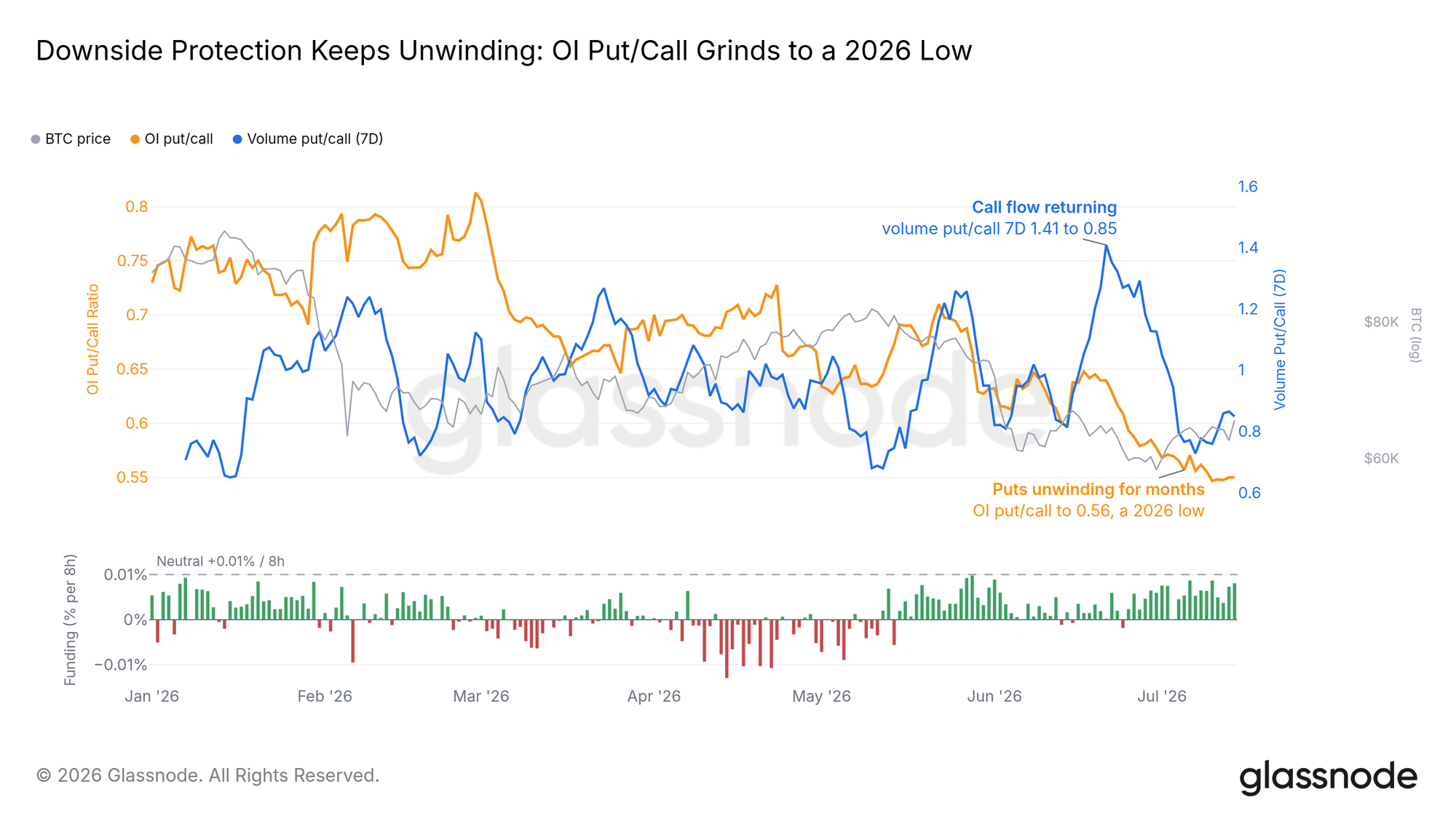

Shorts Give Up the Fight

The derivatives book has been leaning the other way for weeks. The Options Put/Call Ratio has fallen to its lowest of the year as traders let their downside protection expire, and perpetual funding sits just above neutral, nowhere near a crowded long. Bets on further downside are coming off the table, quietly and steadily.

What the unwind has not produced is actual buying. Futures and options traders repositioning is not the same as money entering the spot market, and that absence is the clearest caveat on the whole recovery.

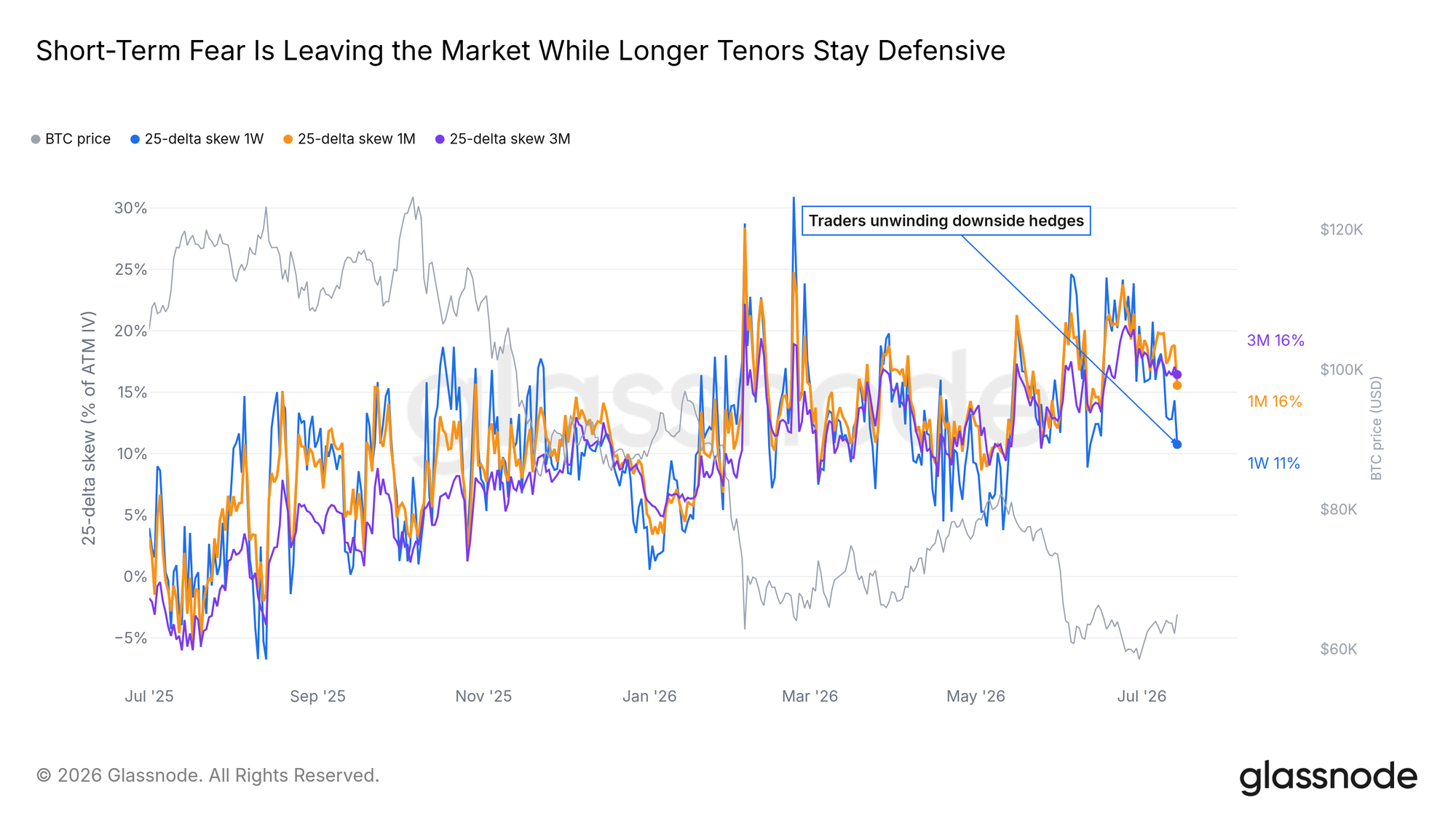

The Fear Premium Eases

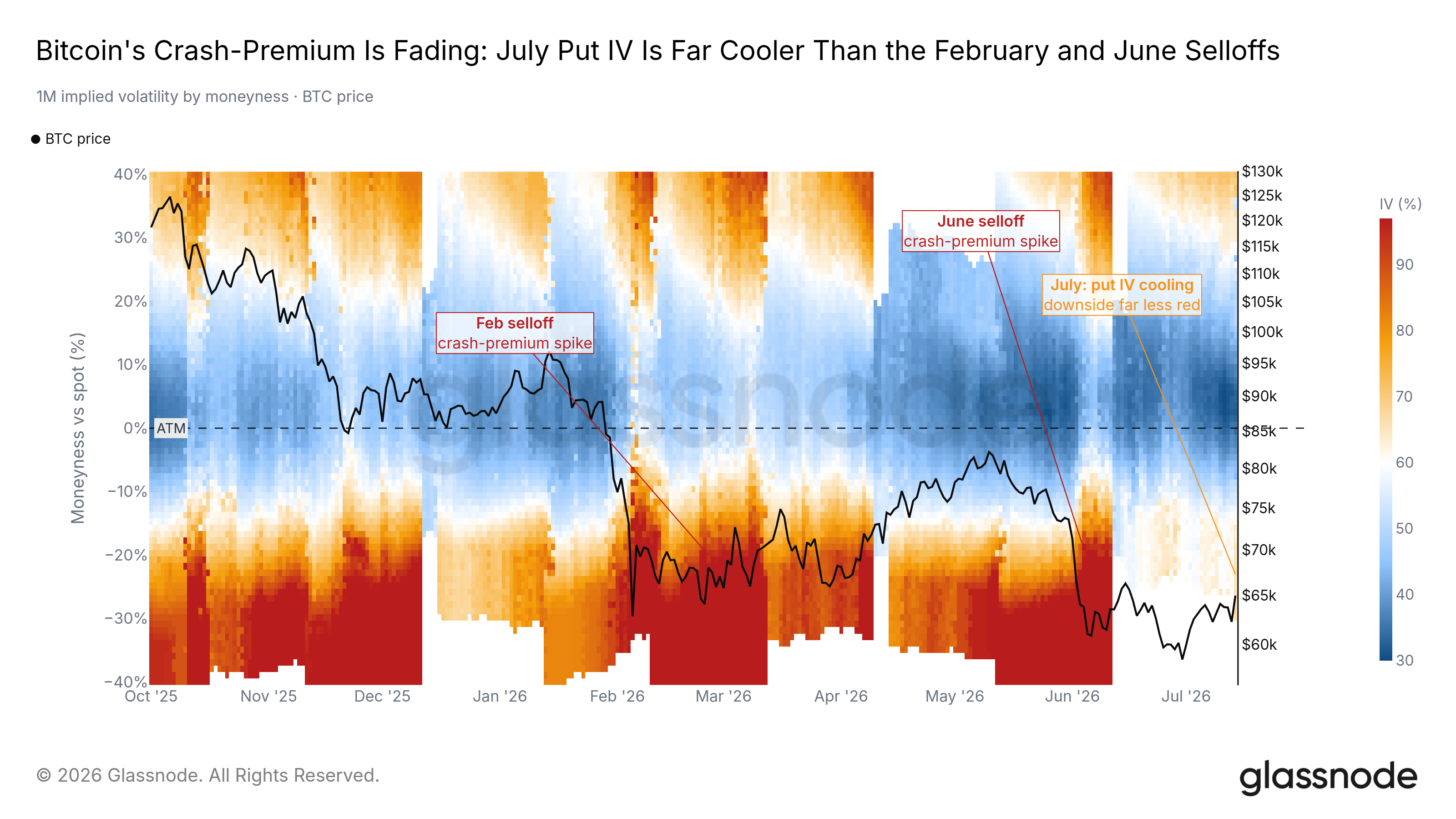

The options market charges a premium for crash protection over upside bets, measured by the 25-Delta Skew. That premium spiked during the June selloff and has been draining since, and it now sits well below its February extreme. Hedging each dip costs less than it did a month ago.

Protection is still bid, as it should be under an unconfirmed low, but the direction of travel is toward normal.

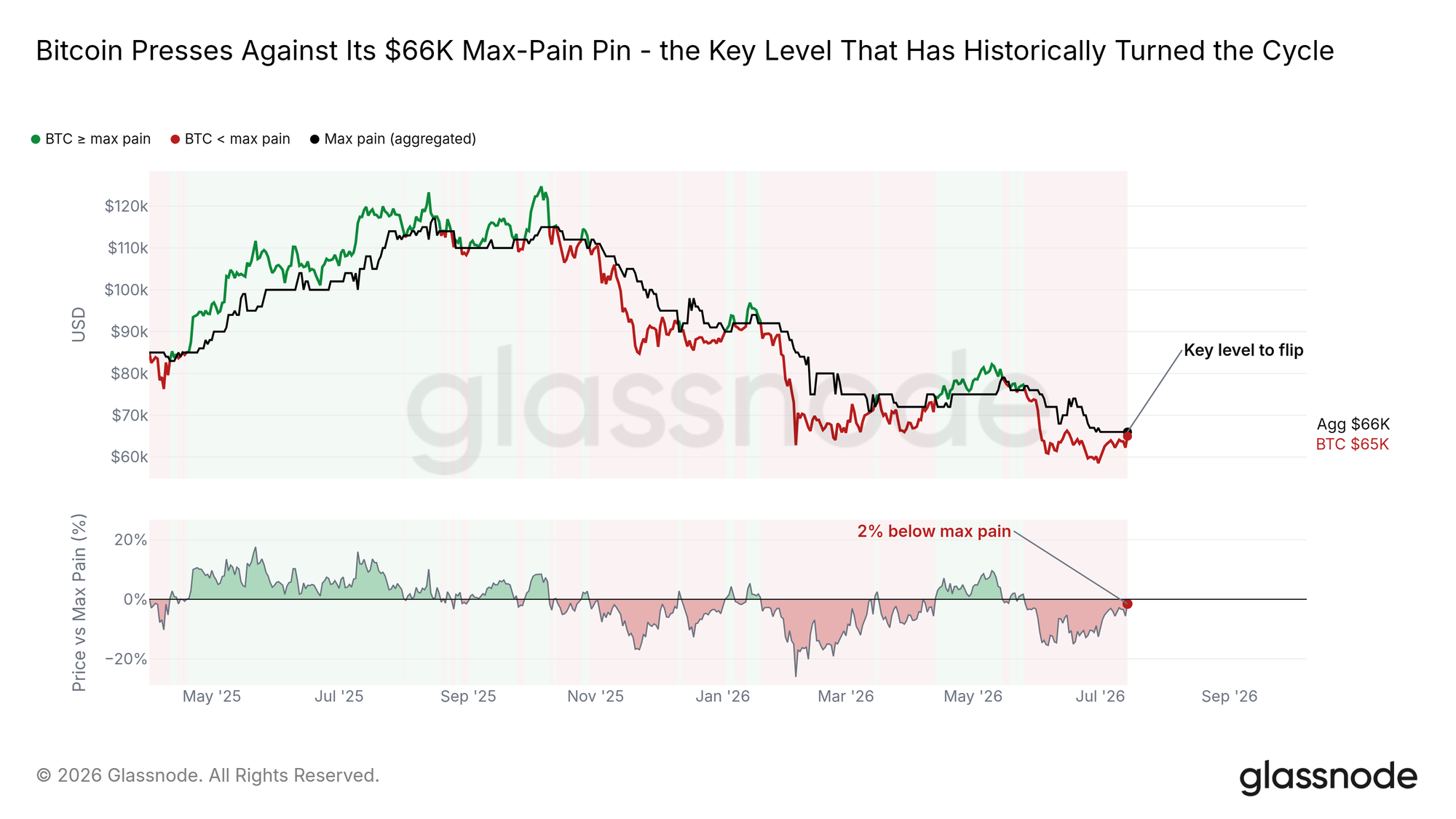

Pressing the Pin

Max pain is the price where the largest share of open options expires worthless, and spot has gravitated toward it all year. Bitcoin now trades just below that level and is pressing against it for the first time in weeks.

Reclaiming the pin has historically lined up with the market shifting back into a friendlier regime, though the flip tends to take time. A clean move above it would be the first structural sign that this range resolves higher; a rejection would confirm the caution still priced into the options market.

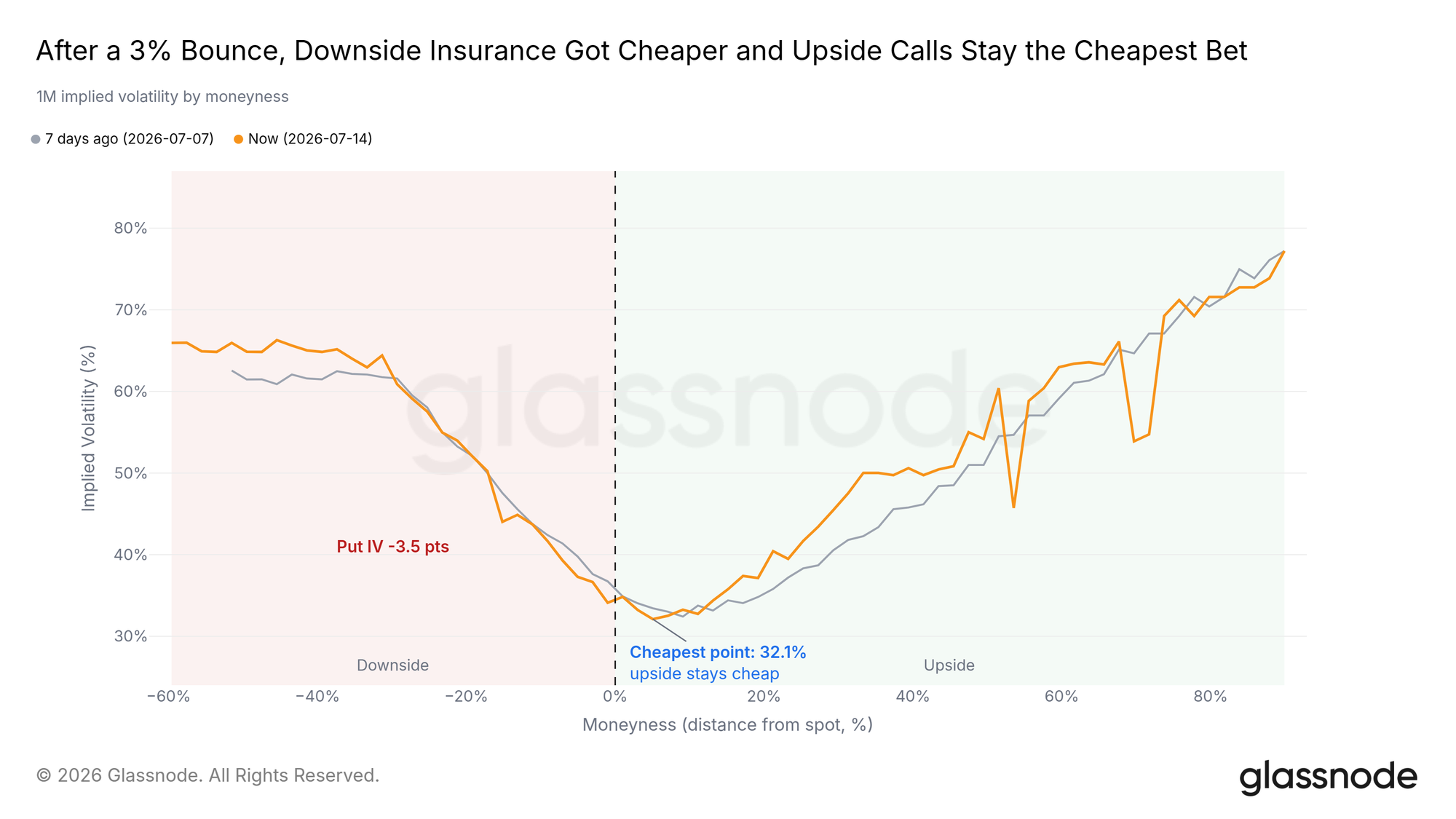

Crash Premium Fades

The absolute cost of protection confirms the easing. Through the recovery, one-month crash protection has repriced steadily cheaper as hedging demand faded. The market still pays up for the downside side of the book, but far less than at the lows.

A Quiet Volatility Regime

The longer view shows how calm the market has become. DVOL, the Bitcoin volatility index, sits near its lowest in a year, and the deep put-side stress that flared in February and June has faded across the surface. Compression like this rarely lasts; it is the backdrop from which the next decisive move usually starts.

Conclusion

The bottom is still building, and this week it started answering back. Long-term holder capitulation has turned down from its peak, profit-taking has dried up, and the June lows were absorbed by broad buying. Bitcoin responded to good macro news more strongly than any other asset, is pressing its max-pain pin from below, and is closing in on the Short-Term Holder Cost Basis above it, where the recovery faces its first real test.

Confirmation is still missing. ETF flows bleed, the derivatives unwind lacks spot follow-through, and volatility sits compressed, waiting for a catalyst. The signal that changes the read is spot-driven buying carrying price through the Short-Term Holder Cost Basis and holding it there. Renewed acceleration in long-term holder losses, or a rejection back toward the Realized Price, sends the market back into its range. The base is built; the follow-through is not.