Diversification Beyond Digital Assets

How the convergence of crypto and private banking is opening doors in both directions.

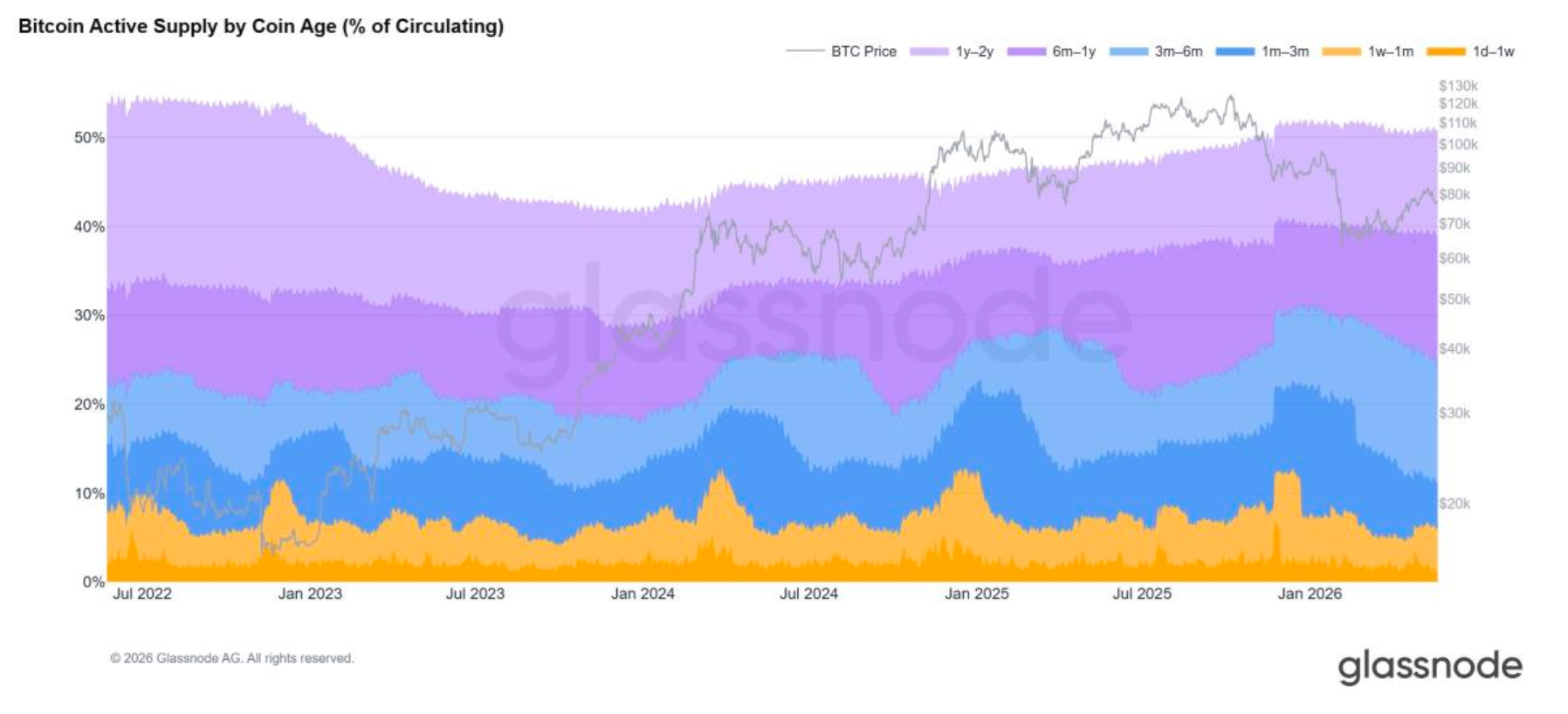

The current phase of the digital asset market is being defined by a clear on-chain signal. As Bitcoin advanced into the cycle peak in late 2025, Long-Term Holders began distributing into strength – a measurable redistribution of supply from seasoned holders to newer market participants. Active Supply rose to 37% of BTC in Q4 2025, while long-dormant supply declined modestly.

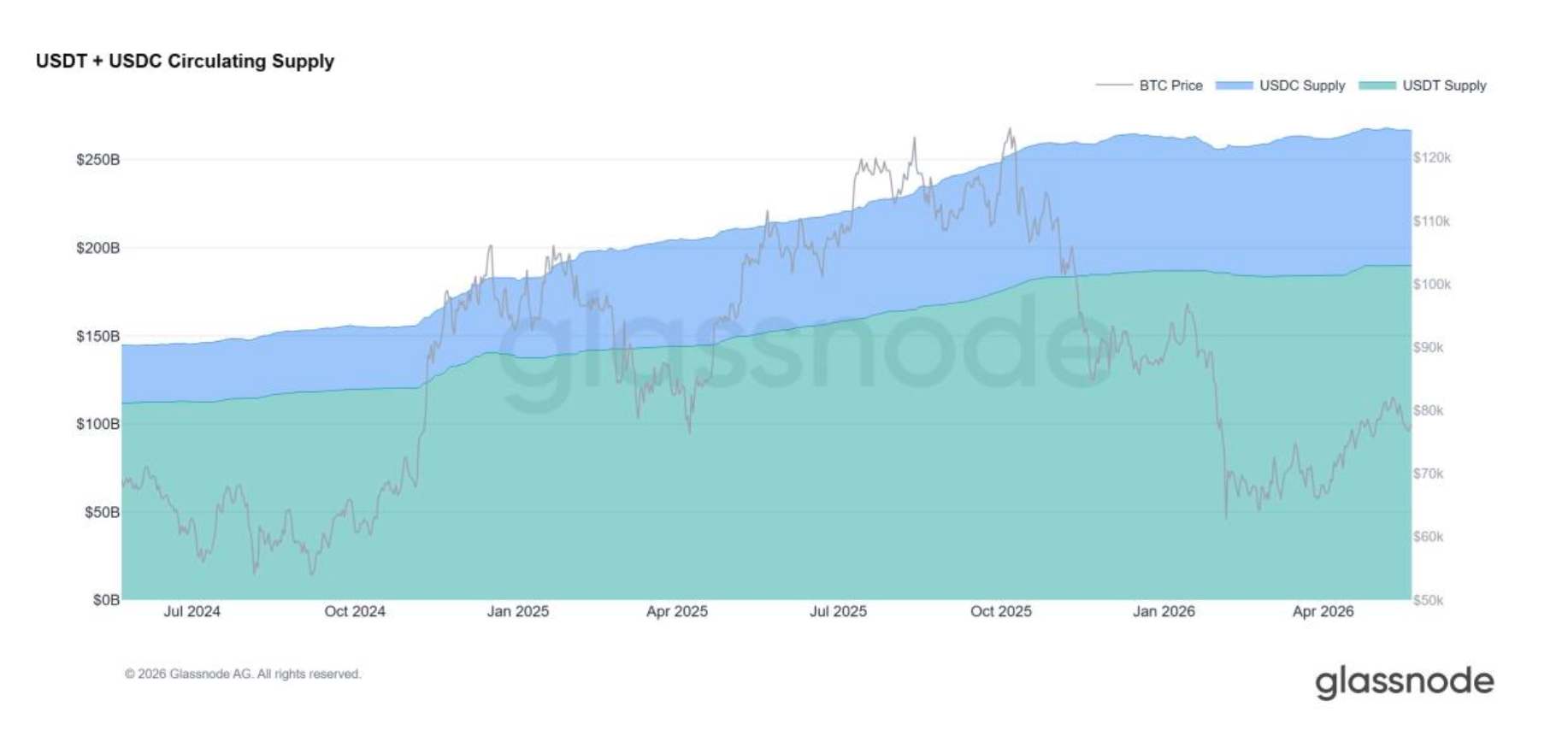

Through the Q1 2026 correction, the picture sharpened further: total crypto market capitalization excluding stablecoins fell by roughly 18%, yet stablecoin supply grew from $308B to $318B. Capital was not leaving crypto markets – it was rotating into cash-like instruments while awaiting clearer signals.

This is what wealth-cycle maturation looks like in the data. Early accumulators are realizing significant capital. New cohorts of buyers - institutional, corporate, and increasingly traditional wealth - are stepping into that supply. The result is the most concrete handover of crypto wealth between cohorts the asset class has ever seen, and it is happening at the same moment that private banking infrastructure is finally beginning to engage with digital assets seriously.

For private banks and wealth managers, this represents a structural opportunity. The HNIs realizing profit are not exiting the asset class - they are looking to diversify, manage liquidity, and access the full wealth-management stack: equities, fixed income, private markets, lending, succession planning. The dynamic also moves in the other direction. As banks become more open to crypto-native clients, they bring new capital and new buyers into digital assets, deepening the institutional demand base that has already absorbed a record share of Long-Term Holder distributions. The flow runs both ways.

The constraint, however, is operational. Effective movement of wealth between digital assets and the banking system depends on one thing: transparent, auditable wealth provenance.

Compliance is the Operational Layer

Private banks were not originally built for clients whose wealth histories sit primarily on a public ledger. Even sophisticated, fully legitimate crypto-native HNIs routinely encounter onboarding friction, repeated information requests, or extended delays as institutions seek clear visibility into the origin and legitimacy of digital assets. To address this - and to allow value to move in both directions between crypto wealth and traditional finance – Glassnode spun out Cense in 2023.

According to Michiel Hoogenboom, Chief Commercial Officer at Cense, the issue is structural rather than procedural. “This goes beyond compliance inconvenience - it is a wealth management issue. When crypto wealth cannot enter the banking system cleanly, the client remains concentrated in a single asset class and unable to deploy capital as efficiently as the overall wealth profile should allow. The same friction also blocks the reverse flow - banking clients who want to allocate into digital assets cannot do so through their trusted institutions.”

Cense leverages the same on-chain analytics foundations that power Glassnode's institutional market intelligence, applied at the client level. Translated into a wealth-management context, that rigor produces auditable, bank-ready documentation of digital wealth histories, a cleaner entry point into private banking and a credible pathway for traditional capital to move the other way.

Benefits Flow in Both Directions

Once crypto wealth becomes bankable, the advantages compound on both sides.

HNIs gain the ability to diversify beyond digital assets, access broader investment opportunities, manage liquidity across traditional and crypto portfolios, and unlock the operational dimensions of private wealth - lending, structured solutions, succession. Private banks, in turn, gain access to a compliant, high-quality deposit base and a durable channel for long-term AUM growth.

The institutional backdrop reinforces the logic. Digital asset markets entered 2026 on firmer footing after last year's deleveraging, with Bitcoin retaining structural leadership. Q2 2026 added nuance: 82% of surveyed institutions now place the market in a bear or late-bear phase, up from 31% in December - yet the rotation into stablecoins and the recovery in BTC derivatives open interest, particularly in perpetuals, point to a rebuilding of risk appetite within the asset class. Institutional allocators are repositioning, not withdrawing.

“Crypto wealth becomes significantly more valuable when it is fully bankable. Once a client has a clean route into private banking, they can diversify beyond crypto, access broader investment opportunities, and manage liquidity across digital and traditional assets. And once banks have a clean route to onboard crypto-native wealth, capital starts moving the other way too.”

- Michiel Hoogenboom, Cense

Looking Ahead: Convergent Wealth

The coming years are likely to be defined less by “crypto versus traditional finance” and more by the convergence of the two - a wealth landscape where HNIs hold a mix of crypto, equities, fixed income, private markets, and cash, and where institutions are equipped to move capital fluidly between them.

The on-chain signal is consistent with this view. The redistribution of supply from Long-Term Holders to new participants through 2025 and into 2026 is, in effect, the largest cohort handover in Bitcoin's history. The capital absorbing it is increasingly institutional. The infrastructure connecting it back to the broader wealth-management stack is where the bottleneck still sits.

“Markets will continue to fluctuate,” Hoogenboom concludes, “but the structural advantages of proactive preparation remain. Investors and institutions who invest the time now to build transparent crypto readiness will be best positioned when conditions accelerate again. Some of Europe's most forward-looking banks - including Van Lanschot Kempen, a leading Dutch private bank - are already on this path. That is a vote of confidence not just in Cense, but in the entire crypto ecosystem's transition into mainstream wealth management.”

About Cense

Cense is a Swiss crypto intelligence specialist, founded in 2023 as a spinout of Glassnode. Its first design partner was a Swiss crypto-native financial institution, where the most complex use cases surfaced early. Today, Cense operates as an independent crypto-intelligence partner between digital asset holders and leading retail and private banks, with a focus on compliance, onboarding, and risk intelligence.

Start a conversation with the experts at Cense.

Disclaimer: This report is for informational and educational purposes only. The analysis represents a limited case study with significant constraints and should not be interpreted as investment advice or definitive trading signals. Past performance patterns do not guarantee future results. Always conduct thorough due diligence and consider multiple factors before making investment decisions.