BTC Market Pulse: Week 25

$BTC rebounded from a low near $60K as selling pressure eased and options markets unwound fear. But with volume, open interest, and capital flows still declining, the move appears more like stabilization and base-building than a confirmed reversal.

Overview

Bitcoin is staging a tentative relief bounce from deeply oversold conditions, but the structural evidence points to stabilization rather than trend reversal. The defining development of the past week is a dramatic shift in taker aggression: Perpetual CVD reversed from -$770M to +$182M and Spot CVD flipped from -$205M to near breakeven. Price momentum confirms this, with RSI climbing 94.8% off extreme oversold levels, yet at 29.1 it remains pinned near its lower statistical band, short of any sustained buyer dominance.

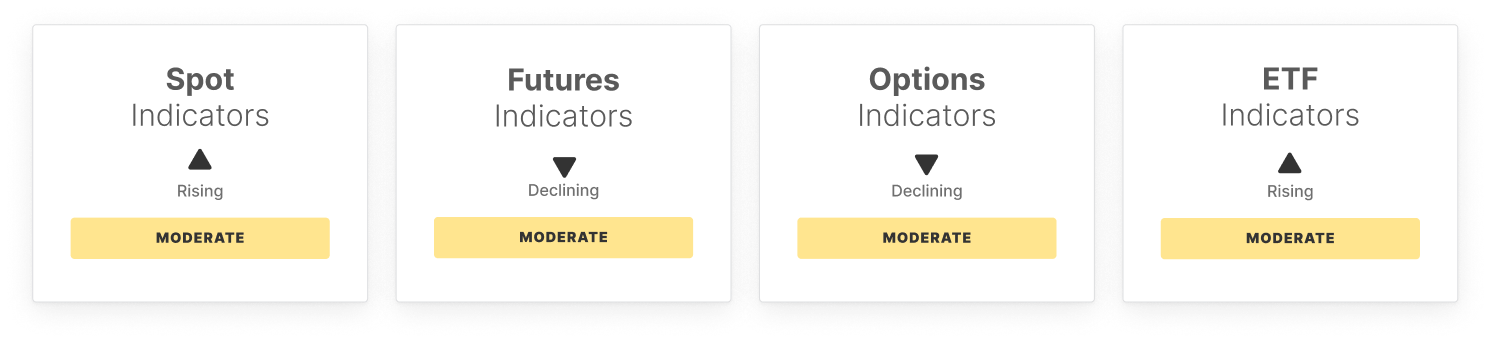

The recovery is happening on thin ice. Spot volume collapsed 40.4% to $5.8B and Futures Open Interest declined another 3% to $30.6B, a sign the bounce is being driven by covering rather than fresh conviction. Long-side funding payments fell 22.3% and ETF trade volume dropped 38.1% to $11.1B. The market is lighter, not healthier.

Fear is receding nonetheless. The Volatility Spread compressed 85% in a single week, from 27.71% to 4.07%, as options participants rapidly repriced tail risk lower. The 25-Delta Skew eased from 19.07% to 15.99%, reflecting reduced demand for downside hedges. ETF net outflows improved 65.5%, narrowing from -$1.3B to -$465M, and the ETF MVRV has crept back above 1.0 to 1.06. Capitulation is decelerating: the Realized P/L ratio improved 46% and the NUPL narrowed 14%, though both remain in net-loss territory.

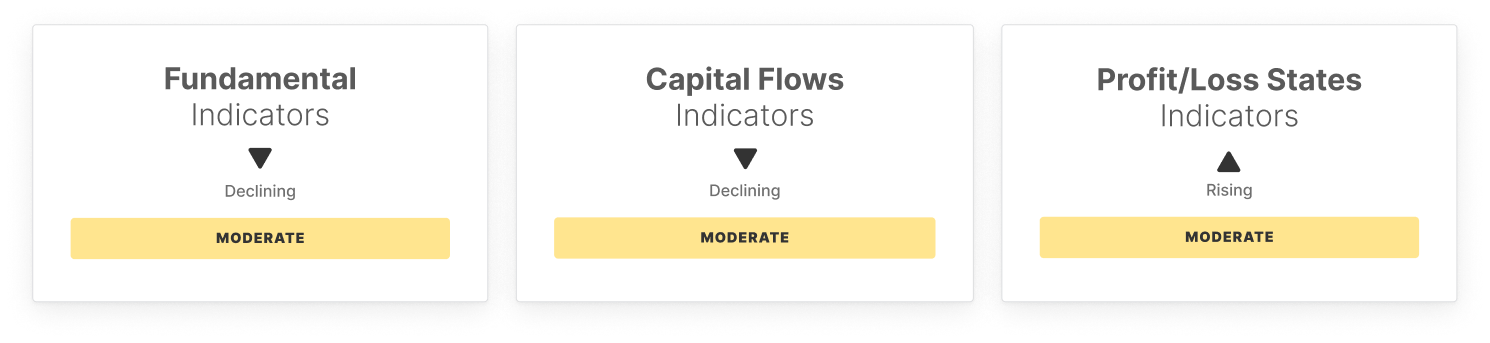

On-chain fundamentals confirm a quieter market. Active addresses fell 6.3% and entity-adjusted transfer volume dropped 38.8% to $3.9B, well below its lower statistical band. Realized Cap Change deepened to -1.3%, signaling that capital continues to exit the network. The one encouraging read is supply composition: Hot Capital Share and the STH-to-LTH ratio have both broken below their lower bounds, indicating that recent-vintage supply has been largely flushed and the holder base is becoming more long-term dominated.

Profitability remains stressed. Just over half the circulating supply (50.8%) is held at a profit, below the 55.1% low band, suppressing sell-side pressure while extending the duration of investor stress.

Capitulation intensity is fading, sentiment hedging is unwinding, and taker behavior has shifted constructively. But the absence of volume, the declining derivatives footprint, and ongoing capital outflows mean this is a consolidation base being built, not a confirmed reversal. Conviction and institutional re-engagement remain the missing catalysts.

Off-Chain Indicators

On-Chain Indicators

🔗 Access the full report in PDF

- Follow us and reach out on X

- Join our Telegram channel

- For on-chain metrics, dashboards, and alerts, visit Glassnode Studio

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.

Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses. We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies.

Please read our Transparency Notice when using exchange data.